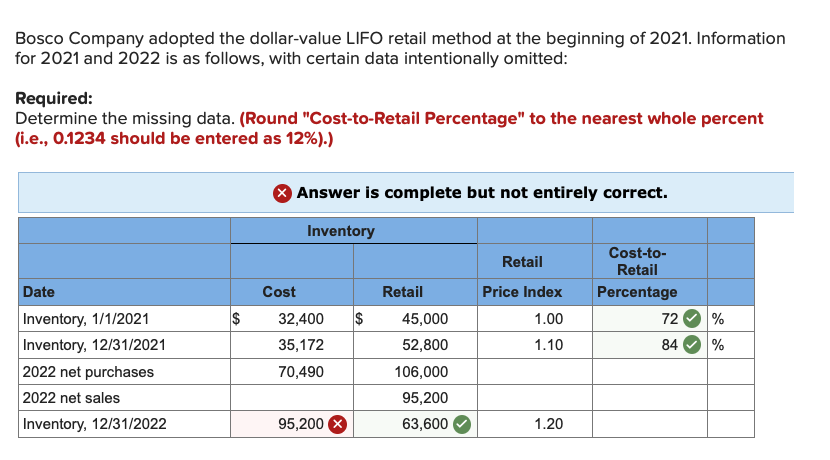

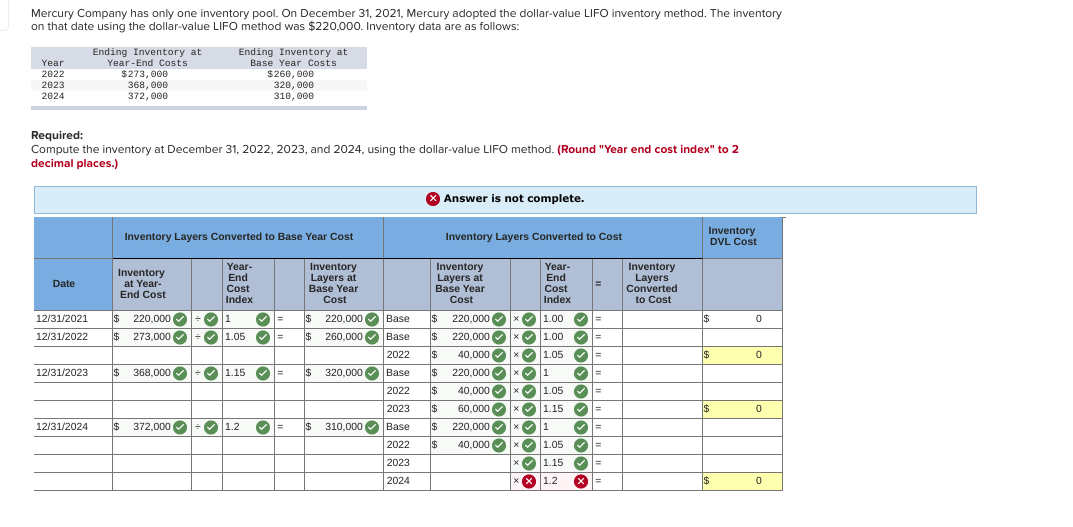

3 2 LIFO methods

In simple words we will have one total figure of all the different types of inventory we like to have in one pool. Dollar-value LIFO is a modification of traditional LIFO method in which ending inventory is measured on the basis of monetary value of units instead of quantity of units held. The base year is 2021, and you have 100 units in inventory that you purchased for $10 each, so your total base-year inventory cost is $1,000.

Why Use the Dollar-Value LIFO Method?

- It essentially shows the proportion of the cost of a certain set of goods in a particular year to their cost in the base year.

- By the end of the year company had 1000 units of Item 1 and 5000 units of Item 2.

- Remember, this is a simplified example and doesn’t take into account some of the complexities that can arise when you have multiple inventory pools or when prices decrease.

- The cutting-edge technology and tools we provide help students create their own learning materials.

- For purposes of this section, a taxpayer is an eligible small business for any taxable year if the average annual gross receipts of the taxpayer for the 3 preceding taxable years do not exceed $5,000,000.

The fashion and apparel industry is a fine example where the Dollar Value LIFO formula can be applied. This industry typically deals with an extensive mix of products, with evolving designs each season, making the Dollar Value LIFO method an ideal approach to inventory valuation. The diversity in products in inventory pools allows this industry to smoothly transition from one year’s collection to another, without dealing with eroding layers. It helps the companies to account for the impact of inflation on their financial reporting. The adoption of Dollar-Value LIFO can lead to significant changes in a company’s financial statements, particularly in the balance sheet and income statement.

FAR CPA Practice Questions: Issuing Stock, Stock Dividends, and Stock Splits

By using this method, ABC Ltd. accounts for these increased costs in its inventory valuation. The company values its ending inventory at the current, higher market prices. This accounting approach aligns the increased costs of recent inventory acquisitions with the revenue generated in the same period. As a result, the company reports a higher cost of goods sold (COGS) and, consequently, lower profits.

Effective Cash Book Management for Modern Finance

Lastly, remember that the Dollar Value LIFO method requires consistency in terms of inventory pools and computations. You need to maintain the logic of classifying the groups and updating the inventory layers. An inventory pool is a grouping of inventory items based on their physical similarities or general category. When calculating the dollar value of the inventory, all items within the same pool are considered collectively, rather than individually. This aids in remarkably simplifying the computations related to the inventory, accounting for the fluctuations in quantities of items in the inventory. Dollar Value LIFO is defined as the method in which the monetary value of the inventory is considered rather than the physical goods when determining the cost of goods sold.

This decrease in reported profits leads to a reduction in taxable income, thereby potentially optimizing ABC Ltd.’s tax liability under this scenario. The Dollar-Value LIFO method thus helps the company in reflecting the impact of inflation on its financial statements, which is especially beneficial in times of rising costs. The reduction in taxable income and subsequent tax payments can improve operating cash flow. This is a crucial consideration for businesses that prioritize cash flow management. Improved cash flow can provide more flexibility for capital expenditures, debt repayment, and other strategic initiatives.

Impact on Financial Statements

First, a large number of calculations are required to determine the differences in pricing through the indicated periods. Also, under IRS regulations, a base year cost must be located for each new inventory item added to stock, which can require considerable research. Only if such information is impossible how to create 7 multiple streams of income: new guide 2023 to locate can the current cost also be considered the base year cost. Specific Identification is a method that assigns actual costs to individual inventory items. This approach is highly accurate and is often used for high-value or unique items, such as luxury goods or custom machinery.

Another major issue with LIFO is delayering or better known as LIFO liquidation or erosion. To solve delayering problem, we use traditional LIFO’s modified approach called Dollar-Value LIFO. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. There is software that can automate these calculations and provide real-time inventory updates, making life much easier. Choose a suitable price index that truly reflects your inventory’s price change.

Dollar-value LIFO places all goods into pools, estimated in terms of total dollar value, and all reductions or increments to those pools are estimated in terms of the total dollar value of the pool. Dollar-Value LIFO (Last-In, First-Out) is a method of inventory valuation that measures changes in the dollar value of the inventory, rather than changes in the physical quantity of the goods in inventory. The simplified dollar-value LIFO approach involves clubbing the inventory into classes or pools of identical items rather than individually counting each item. These categories or groups are the ones that are published or listed as government price indexes.

The ‘layer’ concept and ‘base-year’ concept are inherent parts of Dollar Value LIFO. So, under the Dollar-Value LIFO method, your inventory at the end of 2022 would be valued at $1,360. Charlene Rhinehart is a CPA , CFE, chair of an Illinois CPA Society committee, and has a degree in accounting and finance from DePaul University.

In 2020, you added inventory worth $20,000, which is a layer on top of the base stock. If you use the year 2020 as a base year, the worth of this layer would be calculated in base-year prices. These inventory pools are a collection of items that are grouped based on their similarities. The controller multiplies this amount by the $15.00 base year cost and again by the 121% current cost index to arrive at a cost for this new inventory layer of $23,595. Lower ending inventory values mean that the total assets reported will be lower.

You don’t base your ending inventory value on the count of items, but rather on the dollar value of those items. In 2022, the price of the items increases to $12 each due to inflation, and you purchase 50 additional units. The Dollar Value LIFO formula helps in deriving an accurate inventory valuation which is crucial for reliable financial statements. It ensures no overstatement of income in periods of inflation, thus saving companies from overpaying tax and enhancing net income.